Live Traffic Views in Langley

Andy Schildhorn • August 28, 2025

The Township of Langley Traffic Cameras for up to date traffic information. Click here

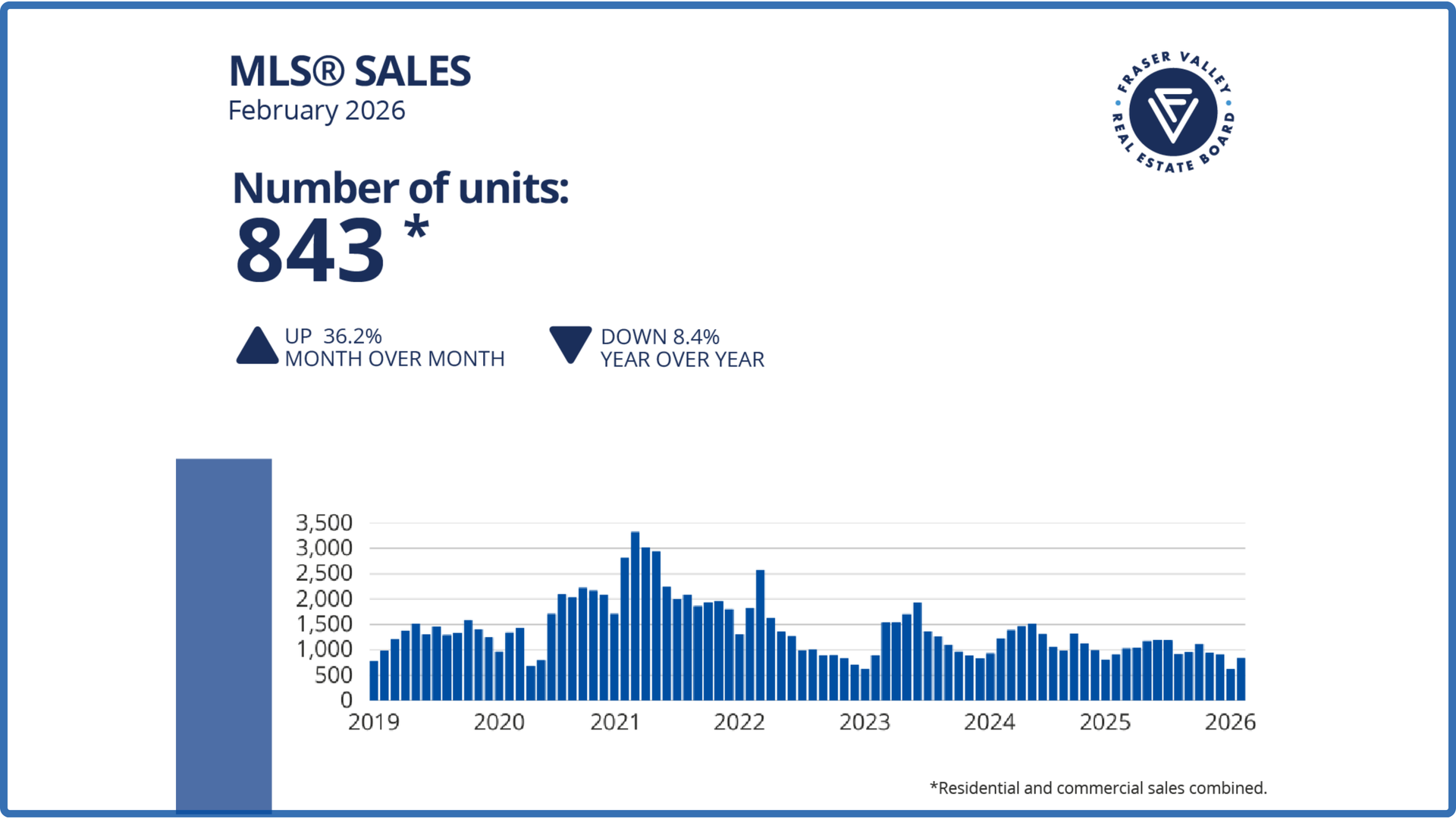

SURREY, BC – The Fraser Valley market showed early signs of a spring thaw in February, with sales increasing over January, but continuing to trail typical levels for this time of year. The Fraser Valley Real Estate Board recorded 843 sales on its Multiple Listing Service® (MLS®) in February, a 36 per cent increase from January, but 38 per cent below the ten-year seasonal average. New listings declined nine per cent in February to 2,796, suggesting some sellers are choosing to wait amid competitive inventory levels, and may be positioning their homes for the peak of the spring market.

The Township of Langley Traffic Cameras for up-to-date traffic information. Click here

The economics of building new homes in Canada are now "simply broken," sparking a macroeconomic drag that CIBC economists warn is just beginning to take hold. 👉 Details Here